In analyzing the alternative financing in Real Estate, we discuss the following;

- Overview of the Real Estate Sector in Kenya,

- Traditional Financing for Real Estate Developments,

- Alternative Financing for Real Estate Developments,

- Case Study: South Africa’s Real Estate Investment Market (REIT) Market,

- Recommendations: Measures to Increasing Access to Real Estate Development Funding, and,

- Conclusion.

Section I: Overview of the Real Estate Sector in Kenya

The Real Estate sector in Kenya has grown over the years to become one of the largest contributors to the country’s Gross Domestic Product (GDP), supported by factors such as; i) positive demographics including higher urbanization and population growth rates of 3.7% p.a and 2.0% p.a, respectively, against the global average of 1.7% p.a and 0.9% p.a, respectively, as at 2023, ii) government’s sustained efforts to promote infrastructural development, opening up new areas for investments, iii) emphasis to provide affordable housing by the government through programs such as the Affordable Housing Program (AHP), iv) increased investment by both local and foreign investors, and, v) increased accessibility to low-interest loans provided by entities such as Kenya Mortgage Refinance Company (KMRC) among others.

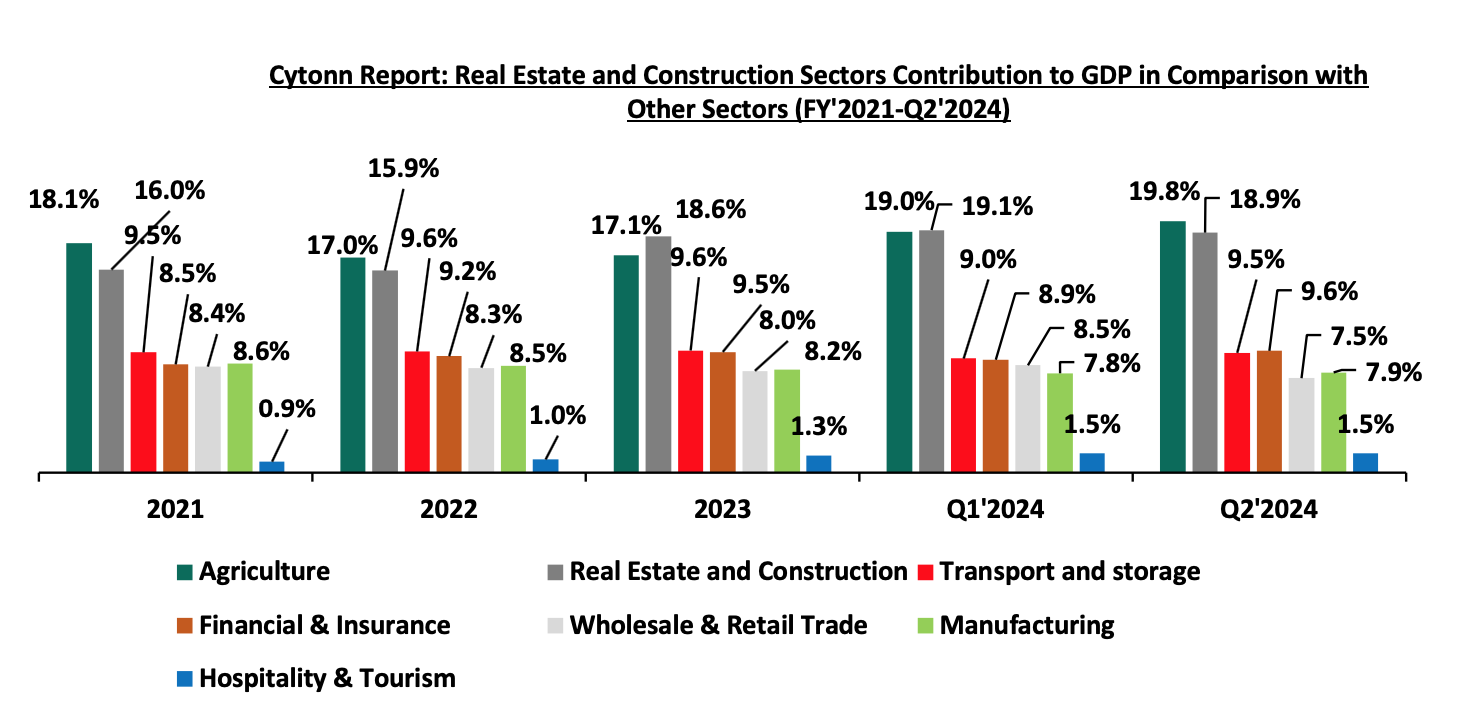

As we assess the growth in the Kenyan property market, it is imperative to recognize the growth achieved by the Real Estate sector, collaboratively with the construction sector, given their interdependence and inherent correlation. Construction and Real Estate sectors jointly contributed to 18.9% to the country’s GDP in Q2’2024, subsequently being the second largest contributors after Agriculture which contributed 19.8%. The performance surpassed major and perennial sector contributors including transport at 9.5%, financial services and insurance at 9.6%, and manufacturing which contributed 7.9%. The performance of the two sectors confirms their importance to the Kenyan economy, and additionally draws a positive outlook. The graph below shows the trend of the Real Estate and Construction sectors contribution to GDP between FY’2021 and Q2’2024;

Source: Kenya National Bureau of Statistics (KNBS)

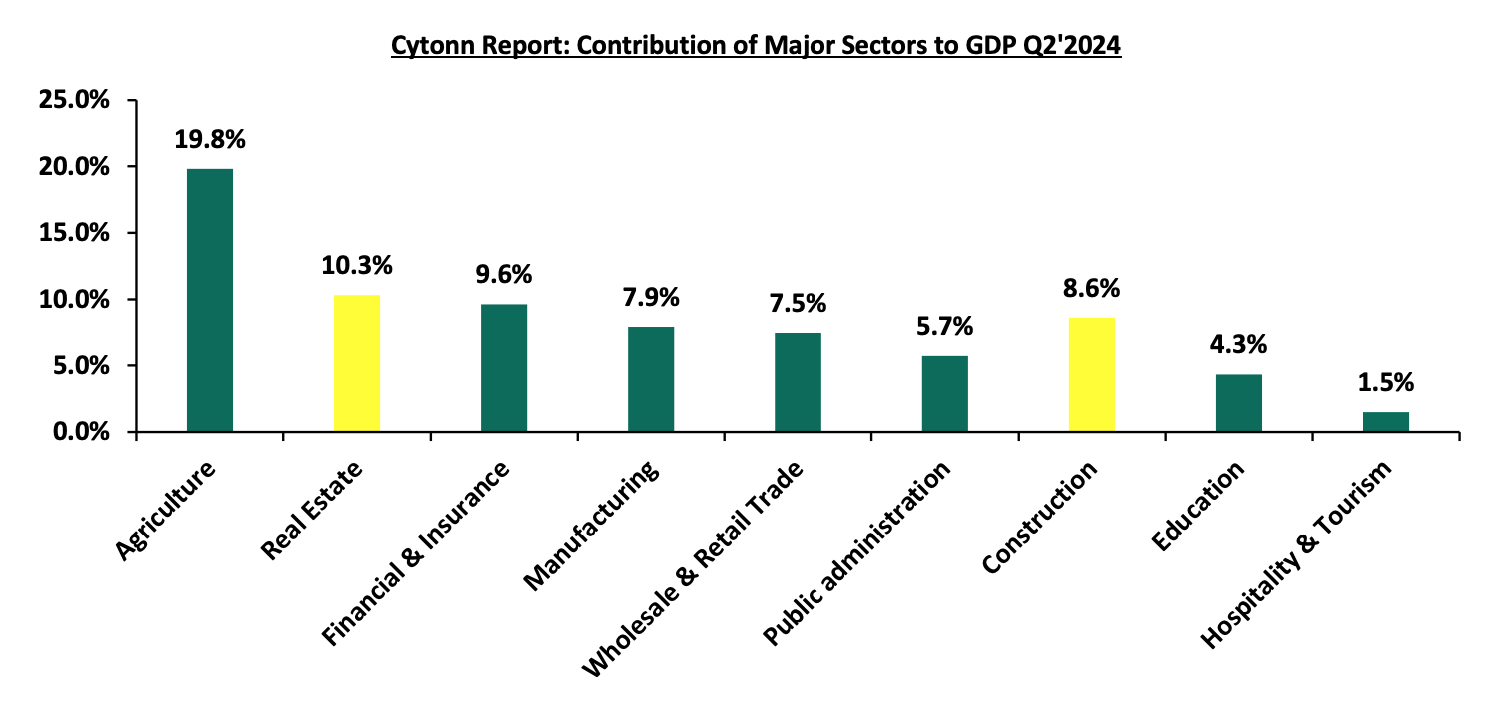

Below is a graph highlighting the top sectoral contributors to GDP in Q2’2024;

Source: Kenya National Bureau of Statistics (KNBS)

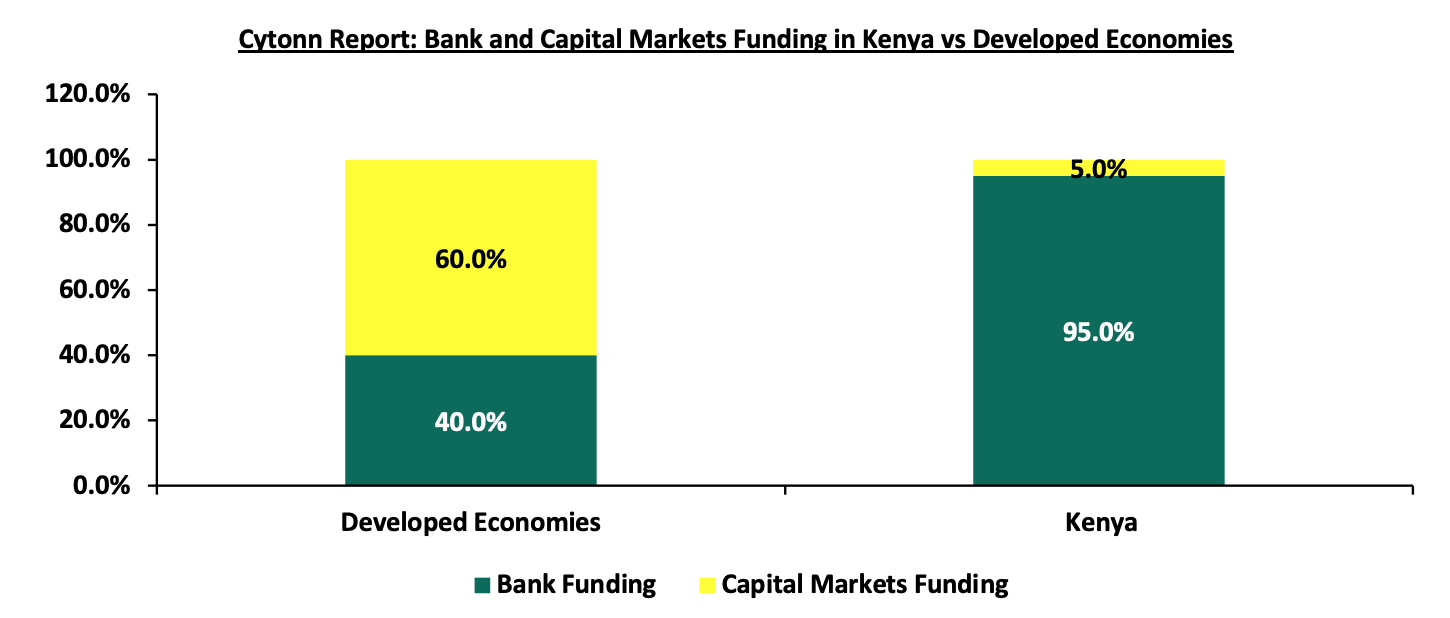

Despite the aforementioned growth and positive performance, several challenges hinder the optimal performance of the Real Estate sector. These challenges include Construction costs which increased by 17.6% in H1’2024, primarily due to higher prices for key materials, which could hinder sector development. Oversupply of physical space exists in various sectors, leading to prolonged vacancy rates. The REITs market in Kenya faces challenges like large capital requirements, prolonged approval processes, and limited investor knowledge. Rising interest rates have made borrowing more expensive, reducing demand for mortgages and developer financing. Lenders are tightening their requirements, leading to constrained financing for developers and an increase in Non-Performing Loans (NPLs) which stands at Kshs 114.3 bn in Q2’2024, equivalent to 22.7% of total loans advanced to the sector. Underdeveloped capital markets limit funding for real estate projects, with banks providing nearly 95.0% of funding for developers in Kenya. To address the funding gap, players in the Real Estate sector have increasingly turned to alternative financing methods like Real Estate Investment Trusts (REITs). In 2013, the Capital Markets Authority (CMA) introduced a detailed framework and regulations for REITs, enabling developers to secure capital through this investment avenue.

Kenya's Real Estate sector has been expanding due to ongoing construction activities driven by strong demand for real estate developments. The residential market is significantly under-supplied, with an 80.0% housing deficit; only 50,000 units are delivered annually against an estimated need for 250,000 units per year. Additionally, the formal retail market in Kenya is still in its nascent stages, with a penetration rate of approximately 35.0% as of 2021. Despite the high demand, developers in Kenya encounter limited financing options, with local banks providing nearly 95.0% of construction financing, in stark contrast to the 40.0% typically seen in developed countries. To bridge the funding gap, developers are increasingly turning to alternative financing methods. The graph below illustrates the comparison of construction financing in Kenya versus developed economies;

Source: World Bank, Capital Markets Authority (CMA)

Section II: Traditional Financing for Real Estate Developments

Real estate development in Kenya is a dynamic sector that demands significant capital investment. Traditional financing methods remain crucial for developers aiming to undertake projects ranging from residential housing to large commercial developments. This article explores various traditional financing options within the Kenyan context, offering detailed insights into their features, advantages, and challenges. These options include:

- Commercial Bank Loans

Commercial banks in Kenya are a primary source of funding for real estate development. These loans are typically structured as long-term debt, with the property often serving as collateral. Prominent banks such as KCB, Equity Bank, and Co-operative Bank offer products specifically designed for developers.

Commercial bank loans are characterized by structured repayment terms that range from 5 to 30 years, depending on the loan size and purpose. Interest rates can be fixed or variable, with the latter often influenced by the Central Bank of Kenya (CBK) base rate. Borrowers are required to provide significant security, commonly in the form of the property under development or other valuable assets. Banks also demand detailed financial records, project plans, and proof of repayment capacity.

These loans provide access to substantial funding for large-scale projects and offer predictable repayment schedules that assist in long-term financial planning. Additionally, the legal frameworks governing such loans protect both parties, ensuring transparency and reliability. This option however, can be challenging since the approval process can be lengthy, involving strict assessments of creditworthiness and project feasibility. For instance, , the interest rate charge average was o 14.3% in 2023, ranging between 8.7% to 18.6% according to Bank Supervision Annual Report 2023, increasing the cost of borrowing, especially during periods of economic volatility leading to increase an in non-performing loans (NPLs).

- Mortgage Loans

Mortgages are a widely used option for financing both real estate purchases and developments. Institutions like Kenya Mortgage Refinance Company (KMRC), Housing Finance Company (HFC) and NCBA cater to residential and commercial real estate developers with tailored mortgage products.

Mortgage loans offer long-term financing options spanning 15 to 25 years. Borrowers may choose between fixed-rate and adjustable-rate mortgages, depending on their risk tolerance and financial forecasts. These loans are secured by the property itself, with monthly repayment plans designed to match the borrower’s income flow. Additional costs, such as valuation, legal fees, and down payments, are factored into the financing arrangement.

Mortgages provide affordable and structured repayment plans, making them suitable for salaried individuals and businesses with stable incomes. Competitive interest rates and the ability to spread costs over an extended period make this a practical choice for many. Despite these advantages, mortgages are faced by challenges such as initial costs, including legal and administrative fees, can be high. Moreover, informal sector earners may face challenges meeting stringent eligibility criteria due to irregular income documentation.

- Construction Loans

Construction loans are designed to fund the building phase of a real estate project. These short-term facilities are common among developers undertaking projects like gated communities, apartments, or commercial complexes. Typically lasting 1 to 3 years, construction loans disburse funds in tranches linked to specific construction milestones. Borrowers are required to present detailed project plans, budgets, and permits before approval. The interest rates on these loans are higher than those of standard loans, reflecting the elevated risk involved in construction projects.

The flexibility of these loans allows developers to access funds as needed, reducing interest costs on unused amounts. This aligns borrowing with project timelines and cash flow requirements.

Developers must ensure meticulous project planning to meet milestone requirements. Transitioning from construction loans to permanent financing upon project completion can also be complex and time-sensitive.

- Bridge Loans and Savings and Credit Co-operatives (SACCOs)

Bridge loans provide short-term financing for developers awaiting long-term funding or the sale of an asset. These loans are particularly useful in Kenya’s fast-growing markets like Nairobi and Mombasa. Bridge loans typically have repayment periods of 6 to 24 months and are secured by existing assets. The approval process is quick, but the interest rates are higher, often exceeding 15.0%. These loans help cover gaps in funding, ensuring projects remain on schedule. These loans are usually offered by banks and non-bank financial institutes. This funding option offer developers rapid access to capital, which is critical for seizing time-sensitive opportunities or maintaining momentum during transitional phases. However, high interest rates and fees make these loans an expensive option. Delays in securing long-term financing can lead to repayment difficulties and increased costs.

SACCOs play a significant role in financing real estate development, particularly for small- and medium-scale developers. Organizations like Stima SACCO and Mhasibu SACCO are known for their competitive loan products. SACCO loans are tied to the member’s savings, typically offering up to three times the savings balance. Interest rates are lower than commercial bank rates, often ranging between 10.0% and 12.0%. Repayment terms are flexible, catering to individual needs. SACCOs promote a savings culture among members while providing accessible loans to those with limited credit histories. The straightforward loan application process is an added benefit. Some of the disadvantages for the SACCOs includes: Loan amounts may not be sufficient for large-scale developments, and the reliance on membership contributions can delay fund disbursement.

- Government-backed Loans and Initiatives

The Kenyan government has introduced various initiatives to encourage real estate development, particularly in the affordable housing sector. Programs under the Kenya Mortgage Refinance Company (KMRC) and the Affordable Housing Scheme are prominent examples. These loans offer subsidized interest rates and extended repayment terms. They are designed to support specific sectors, such as low-income housing. Developers must meet stringent eligibility criteria, including adherence to government-set pricing models. Government-backed loans reduce the cost of borrowing and incentivize socially beneficial projects. They provide critical support for developers focused on addressing Kenya’s housing deficit. The limited availability of funds and bureaucratic processes can slow down approvals and project implementation.

- Equity Financing

Equity financing involves raising capital by selling ownership stakes in a project to investors. This approach is increasingly popular among developers in high-value areas like Westlands and Kilimani. Unlike debt financing, equity financing does not require repayment. Instead, investors share in the project’s profits. Terms are flexible and negotiated between the developer and the investors, often involving detailed agreements on profit sharing and project timelines. Equity financing reduces the developer’s debt burden, allowing them to focus on execution. It also attracts investors with expertise and networks that can enhance the project’s success. Developers, however, must relinquish partial ownership and control. If the project performs exceptionally well, profit sharing may result in higher costs than traditional financing.

In Kenya, traditional financing options provide a robust foundation for real estate development. The choice of financing depends on the project’s scale, risk profile, and timelines. Developers often combine multiple financing methods to optimize their capital structures and navigate the dynamic real estate market. As the sector continues to grow, leveraging these traditional avenues alongside emerging financing models will be critical to meeting Kenya’s housing and commercial needs.

- Pre-Sales

Pre-sales investments involve purchase of properties before or during their construction phases. In Kenya, this approach has gained popularity as it allows investors to acquire properties at prices significantly lower than their anticipated market value upon completion, thereby benefiting from potential capital appreciation. Developers also benefit by securing necessary funding through early sales, facilitating project completion. However, off-plan investments come with certain risks, including: i) Market fluctuations can lead to a decrease in property value by the time of completion, ii) Developers may encounter challenges that delay or halt the project, iii) Investors failing to meet payment obligations can cause project delays or stalling.

In Kenya, the off-plan property market has been expanding, with developers offering various incentives to attract buyers. For instance, some developers provide flexible payment plans, allowing buyers to pay in installments as the project progresses. Additionally, off-plan properties often come with customization options, enabling buyers to influence design aspects to suit their preferences.

Despite these advantages, it's crucial for potential investors to conduct thorough due diligence. This includes researching the developer's track record, understanding the terms of the sale agreement, and assessing the project's feasibility. Engaging with real estate professionals and legal advisors can provide valuable insights and help mitigate risks associated with off-plan investments. While off-plan investments in Kenya offer opportunities for capital appreciation and favorable purchase terms, they also carry inherent risks that require careful consideration and proactive management.

Section III: Alternative financing for Real Estate development in Kenya,

The evolving nature of Kenya’s real estate market has spurred developers to explore alternative financing options beyond traditional methods. These options cater to diverse project needs, offering flexibility and innovative approaches to raising capital. This article examines some of the prominent alternative financing methods in Kenya, detailing their features, benefits, and challenges.

- Private Equity Funding

Private equity (PE) funding has emerged as a viable option for developers seeking substantial capital for large-scale real estate projects. This method involves securing investments from private equity firms or high-net-worth individuals in exchange for a stake in the project. The flexibility of PE funding allows developers to access significant resources without the constraints of traditional loans. Investors often bring valuable expertise and networks, which can enhance project execution and profitability. However, this method requires developers to relinquish partial control of their projects and share profits, which may not appeal to all

- Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts (REITs) represent an innovative financing avenue for real estate development in Kenya. REITs provide a structured mechanism for pooling resources from multiple investors to finance or acquire income-generating real estate assets. The Capital Markets Authority (CMA) regulates REITs in Kenya, ensuring transparency and investor protection. Despite being relatively new in the Kenyan financial market, REITs have shown potential as a transformative tool for real estate financing.

In Kenya, REITs are classified into two main types:

- Development REITs (D-REITs): These focus on financing the construction of new real estate projects. Developers utilize D-REITs to raise capital for large-scale projects, such as residential complexes, commercial buildings, or mixed-use developments. Investors in D-REITs anticipate returns from the eventual sale or lease of the completed properties. Example of this REIT include Acorn D-REIT.

- Income REITs (I-REITs): These are designed for properties that generate consistent rental income. I-REITs appeal to investors seeking steady cash flow from established properties such as office buildings, shopping malls, or industrial parks.In Kenya examples of I-REITs include Acorn I-REIT and Stanbic Fahari I-REITs.

REITs in Kenya are governed by strict regulations aimed at safeguarding investors. They operate as collective investment schemes where a REIT manager oversees the fund's operations. Investors purchase units of the REIT, similar to shares in a company, granting them proportional ownership of the underlying real estate assets. These units are typically traded on the Nairobi Securities Exchange (NSE), providing liquidity and enabling investors to buy or sell their stakes easily.

REITs must allocate a significant portion of their income, often up to 90.0%to investors as dividends, making them attractive to those seeking regular income. Additionally, REITs benefit from tax incentives, such as exemptions on corporate tax, which enhance their appeal to both developers and investors.

REITs offer numerous advantages that make them a compelling option for real estate financing in Kenya:

- REITs provide developers with an efficient way to raise substantial capital without incurring debt. This is particularly beneficial for large-scale projects requiring significant upfront investment.

- By pooling funds from multiple investors, REITs distribute the risk associated with real estate investments. Individual investors are exposed to a diversified portfolio of properties rather than a single project.

- Unlike traditional real estate investments, REITs offer higher liquidity as units can be traded on the NSE. This enables investors to enter or exit their positions with relative ease.

- The mandatory dividend distribution ensures that investors receive consistent returns, making REITs an attractive option for income-focused individuals.

- REITs are managed by experienced professionals who oversee property acquisition, development, and management, reducing the operational burden on investors.

While REITs have significant potential, their adoption in Kenya has been slow due to several challenges:

- Many potential investors and developers are unfamiliar with how REITs operate or their benefits, hindering widespread participation.

- The stringent requirements for establishing and managing REITs can be daunting for developers and fund managers. These include high initial capital requirements and rigorous compliance standards.

- Concerns over transparency and governance have led to skepticism among some investors. Ensuring robust oversight and clear communication is essential to building trust.

- While REIT units are tradable, the relatively low participation in the Kenyan market can limit liquidity, especially during economic downturns.

The future of REITs in Kenya looks promising, especially with increasing demand for affordable housing and commercial spaces. As awareness grows and regulatory frameworks evolve, REITs are likely to play a more significant role in mobilizing capital for real estate development. Government support, including tax incentives and public awareness campaigns, could further stimulate the growth of this sector.

Real Estate Investment Trusts offer a powerful platform for bridging the financing gap in Kenya's real estate sector. By leveraging collective investment mechanisms, REITs provide developers with much-needed capital while offering investors a chance to participate in the lucrative property market. Addressing existing challenges and fostering a supportive environment will be crucial for realizing the full potential of REITs in transforming Kenya’s real estate landscape.

- Crowdfunding Platforms

Crowdfunding has gained traction in Kenya as a modern way to finance real estate projects. Developers leverage online platforms to raise small contributions from a large number of investors. This approach is particularly useful for smaller or community-based projects where traditional financing is challenging to obtain. Crowdfunding allows developers to engage with a broader audience, fostering community involvement and support. However, it requires a compelling pitch and robust marketing to attract investors. Additionally, regulatory frameworks governing crowdfunding in Kenya are still in their infancy, posing risks for both developers and investors.

- Joint Ventures

Joint Ventures (JVs) have become a cornerstone for real estate financing in Kenya, especially in scenarios requiring shared resources and expertise. A Joint Venture is a strategic partnership between two or more entities; typically developers and landowners to co-develop a project and share profits or benefits. These partnerships are particularly prevalent in Kenya due to high land costs and the capital-intensive nature of large-scale projects.

Joint Ventures in Kenya often involve landowners contributing their land as equity, while developers bring the capital, technical expertise, and project management skills. This arrangement minimizes the need for upfront cash investment by developers and ensures that landowners participate in the financial success of the development. Legal agreements outlining profit-sharing, roles, and dispute resolution mechanisms form the backbone of such partnerships, ensuring transparency and trust.

JVs offer a variety of benefits which include: i) Joint Ventures facilitate resource pooling, allowing parties to leverage each other's strengths ii) Developers reduce their financial burden by avoiding land acquisition costs, while landowners gain access to modern developments and potential property appreciation, iii) Furthermore, JVs promote risk-sharing, with each party bearing a portion of the financial and operational risks. Despite their advantages, they often face some challenges which include: i) JVs require meticulous planning and clear communication, ii) Disputes over profit distribution, project timelines, and management decisions are common and can derail projects, and, iv) Additionally, the complexity of drafting equitable agreements often necessitates professional legal and financial advisory, which adds to initial costs. Aligning the interests of all parties is critical to ensuring the venture’s success.

- Islamic Financing

Islamic financing has become an attractive alternative for developers in Kenya, particularly within Muslim-majority regions or communities. This Sharia-compliant financing method prohibits the charging of interest, focusing instead on profit-sharing or lease-based arrangements. Products such as Murabaha (cost-plus financing) and Ijarah (lease financing) enable developers to access funds ethically while adhering to Islamic principles. The growing presence of Islamic banks in Kenya has made these options more accessible. However, the complexity of structuring Sharia-compliant agreements and limited market penetration remain barriers to widespread adoption.

- Venture Capital

Venture Capital (VC) is an emerging financing option in Kenya’s real estate sector, targeting innovative and high-growth projects. Traditionally associated with startups, VC funding has found relevance in developments such as affordable housing and tech-driven real estate solutions.

VC firms provide significant capital to projects in exchange for equity stakes. They often focus on developments with unique value propositions, such as incorporating smart technologies or addressing housing shortages. Unlike traditional lenders, venture capitalists also offer strategic guidance, leveraging their expertise and networks to enhance project viabilityVenture Capital benefits includes: i) VC injects substantial funding into projects, enabling developers to undertake ambitious initiatives that might not be feasible with conventional loans, ii) the collaborative nature of VC funding provides developers access to mentorship and strategic partnerships, iii) the equity-based model means that developers are not burdened with immediate repayment obligations, offering flexibility during early project stages. Despite these advantages various challenges affect venture capital which includes, i) securing VC funding in Kenya remains competitive, with firms prioritizing projects that demonstrate scalability and innovation, ii) the expectation of high returns can exert pressure on developers to achieve rapid profitability. Furthermore, relinquishing equity means developers lose some control over their projects, which may not align with long-term goals

- Green Bonds

As environmental sustainability gains traction, Green Bonds are emerging as a preferred financing option for eco-friendly real estate projects in Kenya. These bonds are designed to raise capital exclusively for projects with environmental benefits, such as energy-efficient buildings and renewable energy integration. Green Bonds operate like traditional bonds but are tied to specific sustainability goals. Issuers must adhere to internationally recognized green bond standards, ensuring transparency and accountability. In Kenya, these bonds are gaining momentum as developers align with global environmental, social, and governance (ESG) trends. Acorn Holdings Limited Green bond was issued in October 2019 and give a return of 12.3% and this bond matured in October 2024.

Green Bonds attract environmentally conscious investors, offering developers access to a niche funding pool. They enhance a project’s marketability by showcasing its commitment to sustainability, which can appeal to tenants and buyers. Additionally, Green Bonds often come with favorable interest rates and government incentives, reducing the cost of financing. This financing option has some demerits such i) the issuance of Green Bonds in Kenya is still in its infancy, with limited awareness among developers and investors, ii) Adhering to stringent certification processes and standards can be time-consuming and costly iii) Furthermore, demonstrating measurable environmental impact requires robust monitoring systems, which can increase project complexity and costs.

Alternative financing options are reshaping Kenya’s real estate landscape, offering developers innovative ways to fund their projects. While each method has unique benefits and challenges, their strategic application can provide the necessary capital to drive growth in the sector. As developers continue to navigate an increasingly complex market, a balanced approach combining traditional and alternative financing methods will be essential for long-term success. By embracing these innovative methods, Kenya’s real estate sector can achieve sustainable growth while meeting diverse market demands. A strategic mix of these financing approaches can unlock new potentials and drive the industry forward

Section IV: Case study; REITs Performance in South Africa in 2024

- Overview of REITs performance in Sub-Saharan Africa

Real Estate Investment Trusts (REITs) have become a significant component of the real estate markets in Sub-Saharan Africa, offering investors opportunities to participate in the region's property sectors. Below is an overview of the REIT landscape across various Sub-Saharan African countries, including details on their establishment, registered REITs, industry size, and primary investment sectors.

|

Cytonn Report: Distribution of REITs investments in Sub-Saharan Africa |

||||

|

Country |

Year of Establishment |

Registered REITs |

Size of Industry (Mn USD) |

Primary Sectors Invested |

|

South Africa |

2013 |

33 |

21,359.0 |

Diversified, Retail, Office, Industrial |

|

Kenya |

2013 |

4 |

2,547.0 |

Retail, Commercial, Student accommodation |

|

Nigeria |

2007 |

3 |

131.0 |

Residential, Commercial |

|

Ghana |

2018 |

1 |

N/A |

Residential, Commercial |

|

Zambia |

2020 |

1 |

N/A |

Residential, Commercial |

Source: Center of Affordable Housing

The REIT markets in Sub-Saharan Africa are still developing, with South Africa leading in terms of market size and diversity of investment sectors. Other countries are gradually establishing their REIT frameworks, focusing on various property sectors, including commercial and residential real estate.

- REITS performance in South Africa

In 2024, Real Estate Investment Trusts (REITs) in South Africa have demonstrated remarkable resilience and growth, becoming a focal point for investors seeking strong returns amidst global economic uncertainties. The performance of REITs has been influenced by a mix of macroeconomic factors, strategic asset management, and evolving market dynamics.

South African REITs operate within a sophisticated framework regulated by the Johannesburg Stock Exchange (JSE), offering investors exposure to a diversified portfolio of income-generating properties. As of 2024, the market capitalization of the REIT sector has surpassed R 400.0 bn, reflecting robust investor confidence and recovery from previous economic downturns. This recovery is evident in the SA Property Index (SAPY), which has outperformed other asset classes, delivering year-to-date returns exceeding 30.0%.

The sector’s growth has been driven by a combination of favorable monetary policies, including interest rate cuts by the South African Reserve Bank, and strategic adjustments by REITs to optimize asset performance. Lower interest rates have reduced borrowing costs, enabling REITs to enhance their profitability and attract investment.

- Performance Drivers for REITs in South Africa

- Strategic Asset Management: Many REITs have undertaken significant asset optimization strategies, including divestment of non-core properties and reinvestment in high-performing assets. For example, Hyprop Investments has focused on bolstering its retail property portfolio, aligning with consumer demand shifts and improving occupancy rates. Similarly, Growthpoint Properties has diversified its portfolio geographically, leveraging its presence in both local and international markets.

- Interest rates and inflation: The reduction in interest rates has played a pivotal role in the sector’s resurgence. Lower rates have decreased the cost of debt, improved net operating income, and enhanced the overall value of property portfolios. Additionally, REITs in South Africa have shown resilience against inflationary pressures by adjusting rental agreements and incorporating rent escalations to maintain steady revenue streams.

- Sectoral shifts: Retail and industrial properties have emerged as high-performing sectors within the REITs space. Retail REITs have benefited from increased consumer spending, while industrial REITs have capitalized on the growing demand for logistics and warehousing facilities, driven by the e-commerce boom. Conversely, office spaces continue to face challenges due to remote work trends, prompting REITs to repurpose or reimagine these assets.

Despite their strong performance, South African REITs have encountered challenges, including; i) fluctuations in the global and domestic economy have created volatility in property valuations and rental income streams, ii) rising utility and maintenance costs have exerted pressure on profit margins, iii) adhering to stringent JSE listing requirements and tax regulations requires robust governance and financial planning ,and, iv) Certain segments, such as office spaces, continue to grapple with elevated vacancy levels, necessitating innovative leasing strategies

- Key players and their strategies

- Growthpoint Properties: Growthpoint remains a market leader, with a diversified portfolio spanning retail, office, and industrial properties. In 2024, the company announced significant investments in mixed-use precincts to address evolving tenant demands. Despite a 10.0% decline in annual distributable income due to high interest rates, Growthpoint’s strategic initiatives signal long-term growth potential.

- Hyprop Investments: Hyprop has outperformed expectations by focusing on retail assets, achieving higher foot traffic and sales turnovers in key shopping centers. Strategic disposals and reinvestments have enhanced its financial position and operational efficiency.

- Attacq Limited: Attacq has prioritized precinct developments, leveraging its expertise to create integrated, sustainable urban spaces. The company’s emphasis on mixed-use developments has positioned it favorably in the market.

South African REITs have showcased their ability to navigate complex market dynamics, delivering impressive returns and reaffirming their value proposition to investors. By embracing innovation, sustainability, and strategic asset management, REITs are poised to continue their trajectory of growth, contributing significantly to the country’s economic development. The outlook for South African REITs in 2024 and beyond remains positive. Key factors shaping the future of the REITs includes; i) increasing focus on ESG (Environmental, Social, and Governance) criteria will drive investments in green buildings and energy-efficient properties, ii) adoption of PropTech solutions will streamline operations and improve tenant experiences, and, iii) expanding into emerging sectors such as data centers and healthcare facilities offers growth opportunities. While challenges such as potential interest rate fluctuations and economic uncertainties persist, the sector’s adaptability and strategic foresight position it as a resilient and attractive investment avenue.

Section V: Recommendations

Increasing access to funding for real estate development requires a combination of government intervention, private sector innovation, and financial sector reforms. Below are detailed strategies to achieve this goal:

- Enhance government policies and incentives: Tax incentives can provide tax rebates, exemptions, or deductions to developers engaged in affordable housing or green building projects. For example, offering VAT exemptions on construction materials for low-income housing can significantly reduce project costs. Public-Private Partnerships (PPPs) allow governments to partner with private developers to execute large-scale projects, involving cost-sharing arrangements, risk mitigation mechanisms, and easier access to land. Establishing government-managed land banks ensures developers have access to affordable and strategically located land, reducing initial capital barriers. State or national housing funds can be created to provide subsidized loans for developers focused on affordable housing.

- Strengthen financial institutions: Development banks or financial institutions focused on real estate development can offer low-interest loans and technical assistance. Loan guarantee schemes, backed by the government, reduce risk for commercial banks and other lenders, encouraging them to provide credit to developers. Long-term financing products with extended repayment terms align better with project cash flows for real estate projects with long gestation periods. Governments can subsidize interest rates for loans directed toward high-impact real estate projects such as affordable housing or infrastructure-linked developments.

- Promote alternative funding sources: Real Estate Investment Trusts (REITs) allow developers to access pooled investments from multiple investors. Streamlined regulations and tax benefits can make REITs attractive to both local and foreign investors. Crowdfunding platforms connect developers with small-scale investors, allowing them to raise equity or debt capital from a broader pool. Green bonds, issued for environmentally sustainable real estate projects, can attract institutional investors seeking to meet ESG (Environmental, Social, and Governance) criteria. Securitization of mortgages provides banks and financial institutions with additional liquidity to lend to developers.

- Increase transparency and reduce risks: Streamlining and digitizing building codes, zoning laws, and project approval processes can reduce bureaucratic delays and associated costs. Governments must prioritize digitizing land records and expediting the issuance of title deeds to eliminate disputes and instill confidence among lenders and investors. Publicly accessible databases with real-time information on property prices, demand trends, and construction costs enable data-driven decision-making by developers and financiers.

- Encourage capacity building to create awareness: Training programs can be organized for developers on topics like financial planning, risk management, and sustainable construction practices. Advisory institutions or desks within financial institutions can guide developers on structuring projects and accessing funding. Knowledge-sharing platforms can create forums for developers, financiers, and policymakers to share insights and experiences.

- Facilitate access for small-scale developers: Microfinance institutions (MFIs) can develop tailored financial products for small and medium-sized developers to enable them to access affordable credit. Smaller developers can form cooperatives or joint ventures to pool resources and undertake larger projects. Technical and financial advisory support can be provided to small-scale developers to improve their creditworthiness and project management skills.

- Attract foreign direct investment (FDI): Simplifying investment processes by reducing red tape and creating single-window clearance systems for foreign investors can facilitate FDI. Incentives such as tax holidays, repatriation benefits, or preferential treatment in specific zones can attract foreign investment. Actively marketing the country’s real estate opportunities at international forums and trade fairs can also attract global investors.

- Digital innovations in financing: Blockchain can create transparent and secure systems for property transactions and financial records, reducing fraud and improving investor confidence. PropTech platforms can connect developers with lenders, investors, and service providers. Fintech innovations can provide faster, data-driven credit assessments for real estate projects through digital lending.

Implementing these measures can significantly improve access to funding for real estate development. This will not only stimulate economic growth but also address critical housing and infrastructure deficits. Collaboration between governments, private developers, financial institutions, and technology providers is essential to unlock the full potential of the real estate sector.

Section VI: Conclusion

Financial constraints remain a significant hurdle for developers in Kenya, primarily due to the limited availability of diverse financing options. Traditionally, real estate investments have relied on conventional funding sources such as debt financing, equity financing, and personal savings. While these methods have supported many projects, they are often insufficient to meet the growing demand for large-scale developments. To address this issue, developers can consider alternative financing mechanisms that have gained traction globally. These include Real Estate Investment Trusts (REITs), which pool funds from multiple investors to finance income-generating properties; structured financial products such as mortgage-backed securities; and Public-Private Partnerships (PPPs) that leverage collaboration between the public and private sectors to execute projects more efficiently.

Additionally, there is an urgent need for policy reforms to expand the role of capital markets in project financing. In Kenya, capital markets currently contribute a negligible 5.0% to real estate financing, a stark contrast to developed countries where they provide approximately 60.0% of funding. The remaining 40.0% in these markets typically comes from debt financing through banks, highlighting a balanced and robust financial ecosystem.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice, or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.