The Kenyan Shilling has experienced a marginal depreciation of 21.5 bps on a Year-to-Date against the US Dollar, closing the week at Kshs 129.6 as of February 21, 2025, compared to Kshs 129.3 at the beginning of the year. This is a contrast to the 17.4% appreciation in 2024 while in 2023, 2022, and 2021 the currency depreciated by 26.8%, 9.0%, and 3.6% respectively. The appreciation experienced in 2024 and the current stability of the Shilling is supported by improved forex reserves currently at USD 9.3 bn (equivalent to 4.7-months of import cover), an increase of 28.2% from USD 7.2 bn (equivalent to 3.9-months of import cover) recorded in a similar period in 2024, and an 18% increase in diaspora remittances to USD 4,945.0 mn in 2024 higher than USD 4,190.0 mn recorded in 2023 and the ease in inflation, with the current inflation rate as of January 2025 coming in at 3.3%, within the CBK target range of 2.5%-7.5%.

The interest rates have seen significant decreases over the last seven months with the 91-day treasury bill rates getting to a low of 9.0%, the lowest since September 2022. In the Eurobond market, the rates have been low with Eurobonds trading at rates of below 11.0% in February 2025. Interest rates have declined due to reduced government borrowing pressure, driven by improved liquidity conditions, eased inflation, increased external funding, and a shift in debt management strategies. The Kenyan macroeconomic environment challenges have alleviated as evidenced by credit rating outlook revision by Moody’s. In January 2025, Moody’s announced its revision of Kenya’s credit outlook to positive from negative, while maintaining the credit rating at Caa1, on the back of a likelihood of an ease in liquidity risks and improved debt affordability. The improved debt affordability is largely attributable to the reduction in domestic borrowing costs, evident in the sharp decline of yields for short-dated papers. Similarly, Fitch Ratings affirmed Kenya's Long-Term Foreign-Currency Issuer Default Rating (IDR) to 'B-' with a Stable Outlook in January 2025;

We have previously covered the topic as summarized below;

- In January 2024, we covered Currency and Interest Rates Review, with our outlook on the currency being a 16.4% depreciation mainly on the back of the ever-present current account deficit with Kenya being a net importer, which was to increase US Dollar demand in the market, and the persistent US Dollar demand by importers, mainly in the oil and energy sector as well as manufacturers, while the US Dollar supply remains low resulting to a shortage of USD in the Kenyan market. On the interest rates, we expected an upward readjustment on the yield curve due to the increased pressure on the government to meet its budgetary deficit by borrowing more domestically, coupled with uncertainties about the economy occasioned by elevated inflationary pressures which had resulted in high credit risk hampering lending to businesses and individuals.

With the shilling having appreciated by 17.4% at the end of 2024 and the continuous downward readjustment on the yield curve, we saw the need to revisit the topic of currency and interest rates outlook, in order to shed some light on how the Kenyan shilling and the interest rates are expected to behave in 2025. In this focus, we shall be doing an in-depth analysis of the factors that are expected to drive the performance of the Kenyan shilling and the interest rates and thereafter give our outlook for 2025 based on these factors. We shall cover the following:

- Historical Performance of the Kenyan Shilling and Drivers,

- Evolution of the Interest Rate Environment,

- Currency Outlook,

- Factors Expected to Drive the Interest Rate Environment, and,

- Conclusion and Our View Going Forward.

Section I: Historical Performance of the Kenyan Shilling

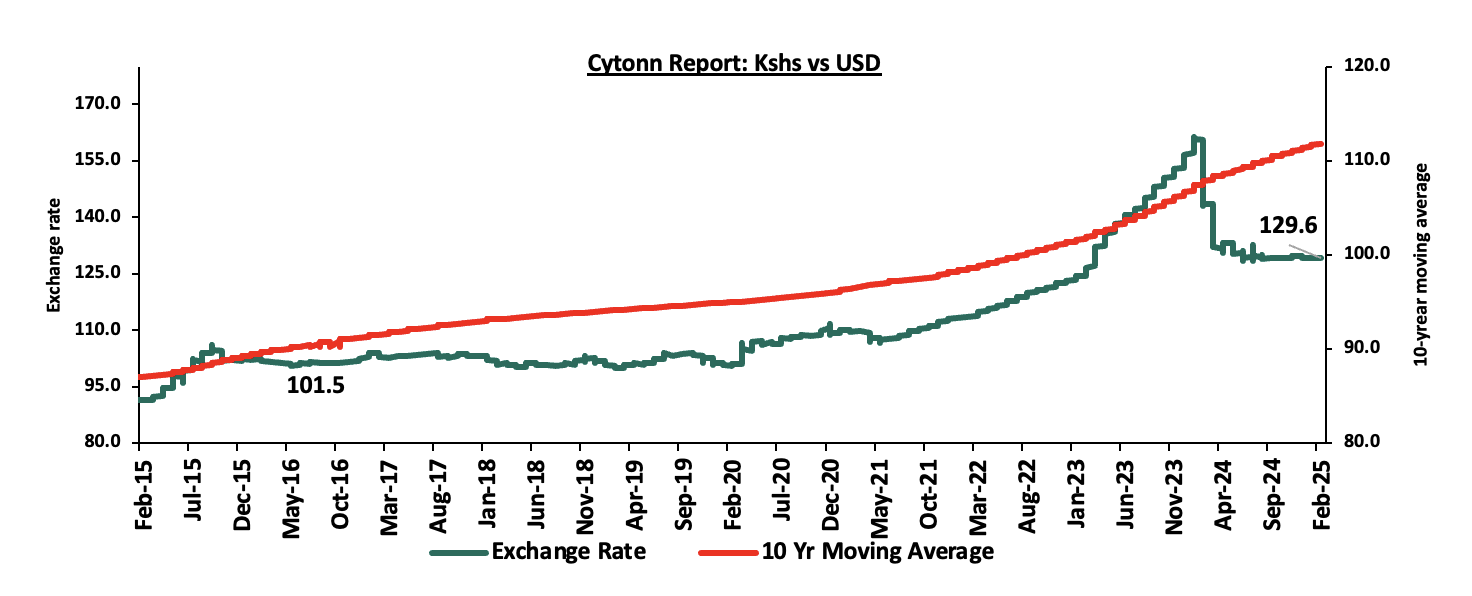

The Kenyan shilling has depreciated at a 10-year CAGR of 3.5% to close at Kshs 129.6 as of 21st February 2025 from Kshs 91.6 over the same period in 2015, mainly attributable to challenges within the country’s macroeconomic environment. Over the last years we have seen the country run a fiscal deficit which has led to the government borrowing both locally and internationally and continues to witness a persistent current account deficit, recorded at 4.0% of GDP as of Q3’2024 projected at 3.7% of GDP for FY’2024, which continues to weigh down the Shilling. The current account deficit is largely due to the high imports of petroleum products and the manufacturing equipment. However, in 2024, the shilling appreciated for the first time in six years, closing the year at Kshs 129.3 against the US Dollar as compared to the Kshs 157.0 at the beginning of the year translating to appreciation of 17.4%, and a contrast to the 26.8% depreciation in 2023, majorly attributable to the Eurobond buyback in February 2024, alleviating credit risk and improving investor confidence, and the improved forex reserves. The chart below illustrates the performance of the Kenyan Shilling against the US Dollar over the last 10 years:

Source: Cytonn Research

The following are the factors that have continued to support the shilling;

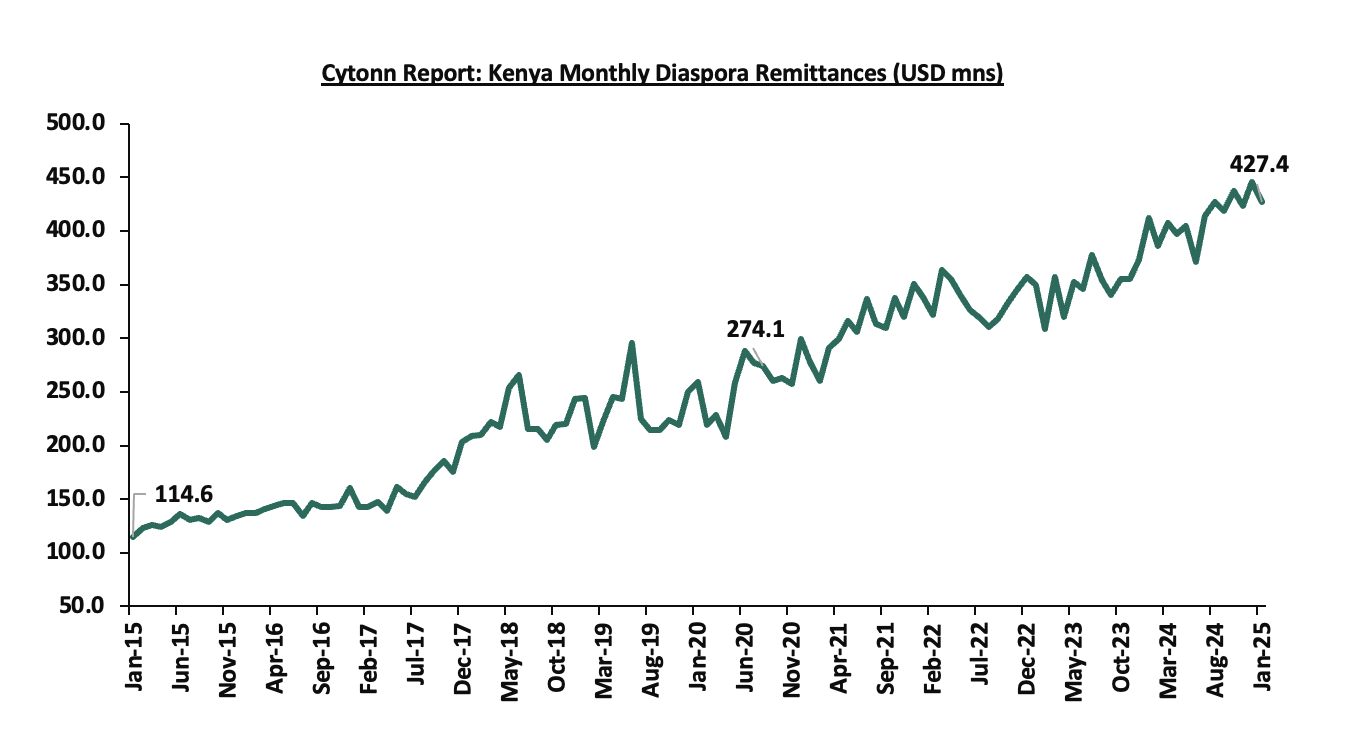

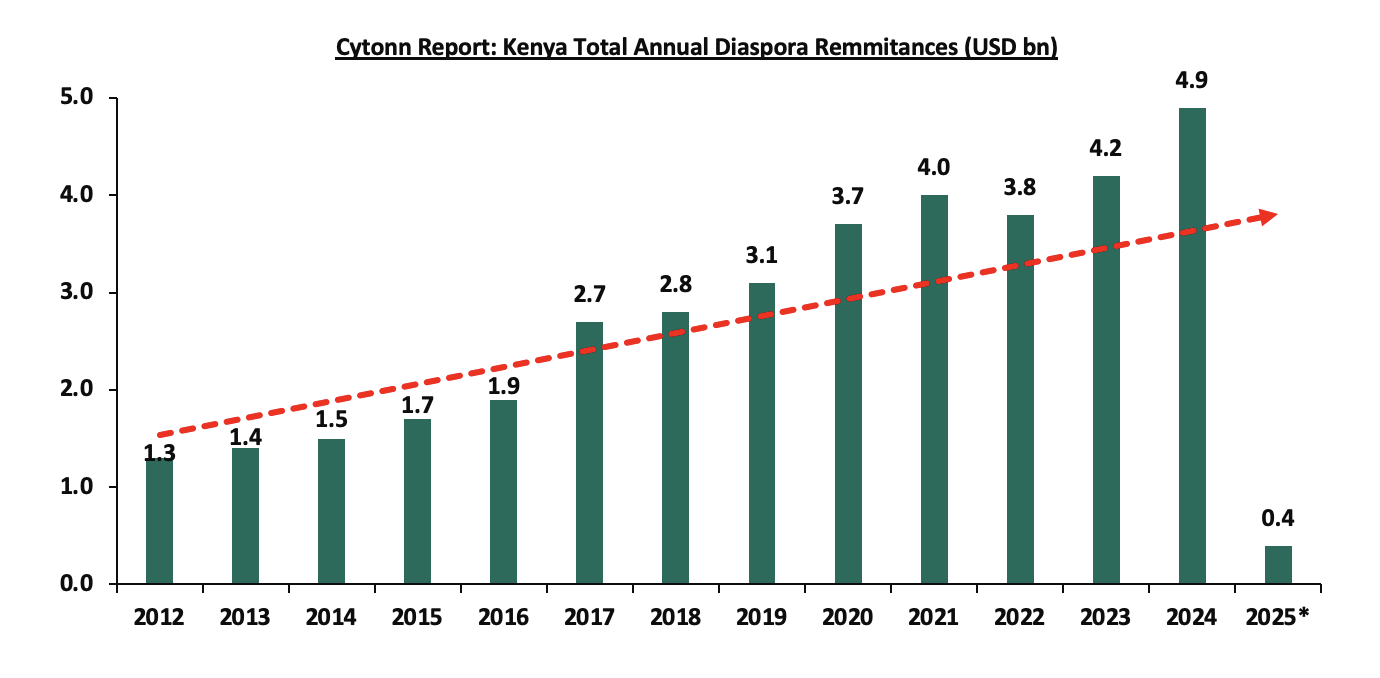

- Strong diaspora remittances, with monthly diaspora remittances having grown at a 10-year CAGR of 14.1% to USD 427.4 mn in January 2025, from USD 114.6 mn recorded in January 2015. In the 12 months to January 2025, the Diaspora remittances stood at a cumulative USD 4,960.2 mn which is 16.6% higher than the USD 4,252.9 mn recorded over the same period in 2024. The continued growth in diaspora remittance is mainly attributable to the recovery of the of the global economy, increasing Kenyan population in the diaspora and advancing technology that has facilitated easier transfer of money. The charts below show the trend of the evolution of monthly and annual Diaspora Remittances;

Source: Central Bank of Kenya

Source: Central Bank of Kenya, * figure as of January 2025

- The narrowing of the current account deficit due to the increased value and volumes of the country’s principal exports relative to the import bill, with total exports increasing by 6.0% in Q3’2024, compared to a 5.0% growth in imports over the same period. It is good to note that there has been a positive trend with the current account deficit coming at 4.0% of GDP in Q3’2024, and projected at 3.7% of GDP for FY’2024. Notably, exports of coffee grew the most by 26.8% in Q3’2024, to Kshs 12.0 mn from Kshs 9.5 mn in Q3’2023. Also, in Q3’2024, tea exports and horticulture contributed Kshs 44.7 mn and Kshs 50.3 mn, respectively, to the total export value of Kshs 282.4 mn. This however, marked an 11.4% decline in tea export earnings from Kshs 50.4 mn in a similar period last year, while horticulture saw a 3.1% increase from Kshs 48.8 mn in Q3’2023,

- Kenya has continued to receive financing from the International Monetary Fund and the world Bank which have supported the Kenyan shilling by boosting the forex reserves. Notably, the government received USD 215.0 mn from the World Bank loan to build resilient and responsive health systems projects in March 2024, as well as USD 485.8 mn from the International Monetary Fund (IMF) in October 2024 under the 38-month Extended Fund Facility (EFF) and USD 120.3mn from Extended Credit Facility (ECF) following the completion of the seventh review and eight review

- The Central Bank of Kenya (CBK) has been actively selling US dollars to the market to smooth out the volatility of the Kenyan shilling. By selling dollars, the CBK matches the demand in the market, mainly by importers, which has continued to shield the Shilling from pressure and helps maintain a stable exchange rate

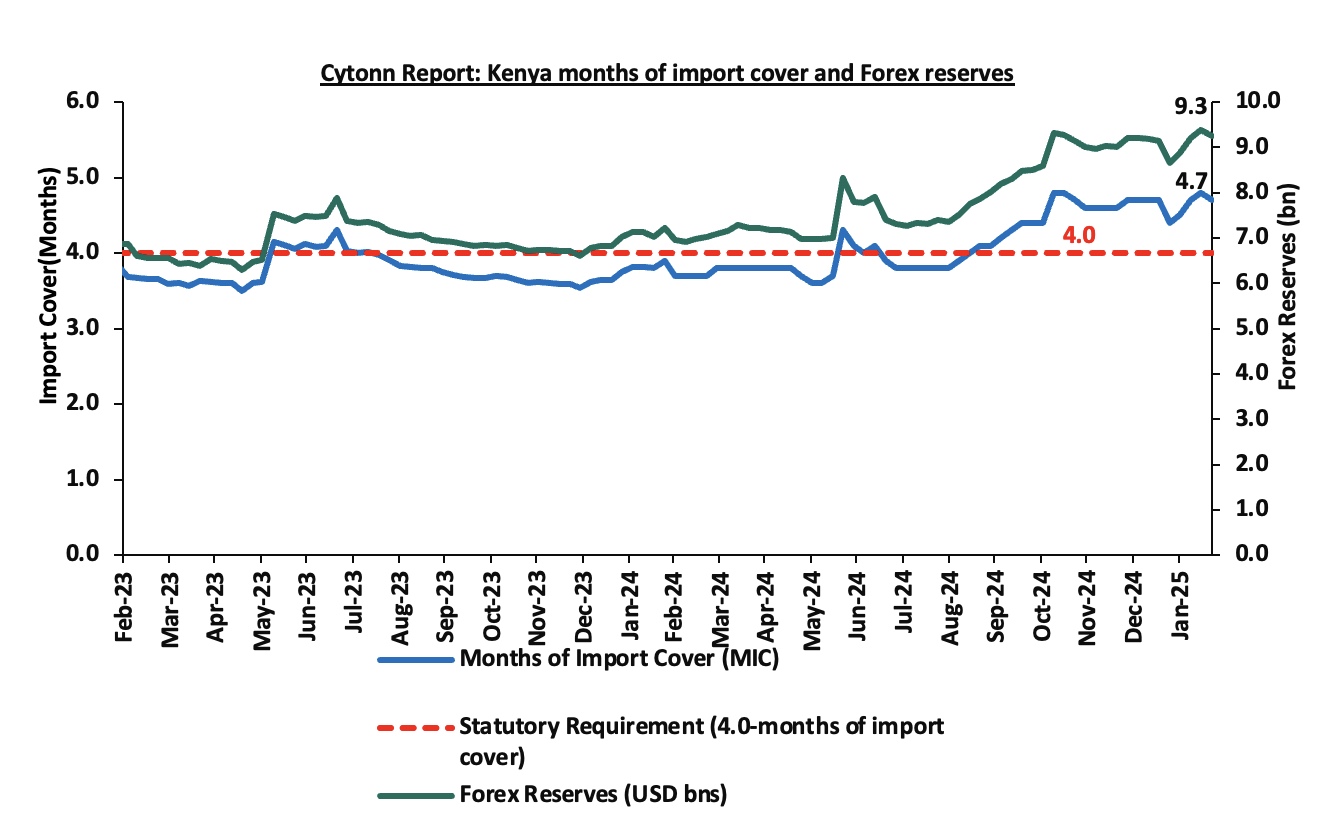

- Improving forex reserves having increased by a significant 28.2% to USD 9.3 bn (equivalent to 4.7 months of import cover) as of 21st February 2025, from USD 7.2 bn (equivalent to 3.8 months of import cover) in a similar period in 2024. Notably, for the last six months, forex reserves have remained above the statutory requirement of maintaining at least 4.0-months of import cover. The increase is largely attributed to decreased debt service obligations due to the continued appreciation of the Kenyan shilling. The chart below shows the trend of the evolution of the forex reserves:

However, the shilling remains under pressure due to;

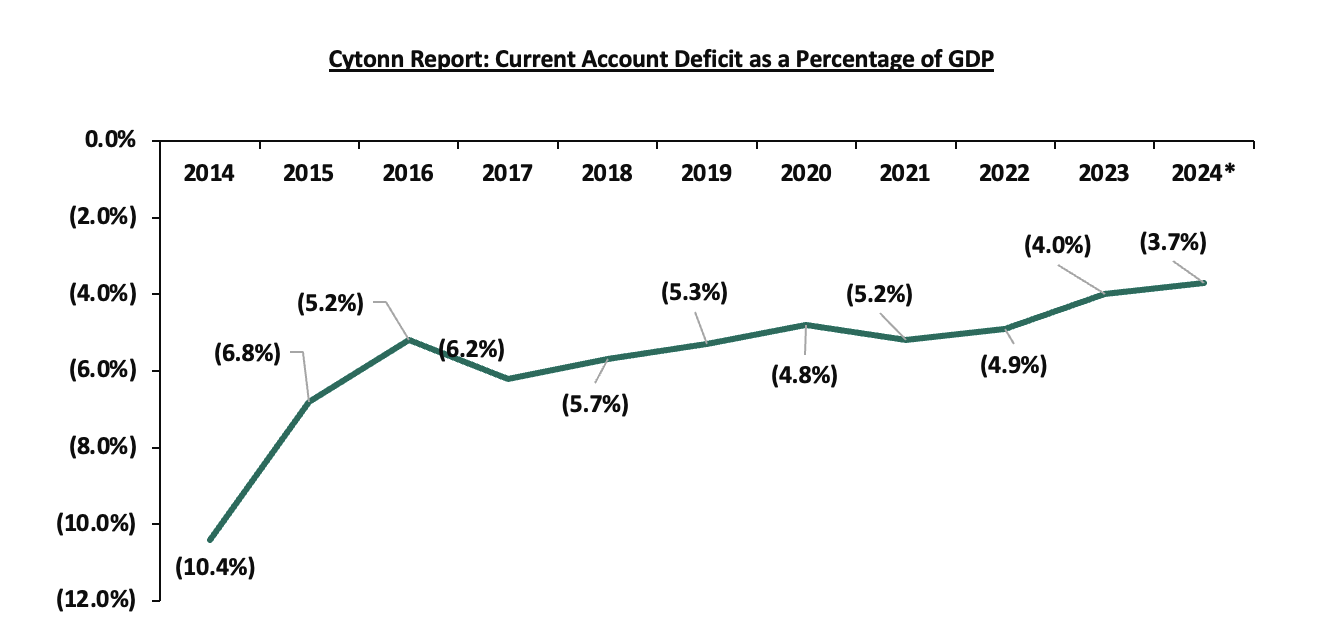

- The existence of an ever-present current account deficit, coming in at 4.0% of GDP as of Q3’2024.The persistent current account deficit highlights the country's dependence on imports. The chart below highlights the trend in the current account deficit as a percentage of GDP for the last 10 years:

Source: Kenya National Bureau of Statistics (KNBS), 2024* data as of Q3’2024

- The low interest rates as evidenced by the expansionary monetary policy stance adopted by the MPC. The Monetary Policy Committee reduced the Central Bank Rate (CBR) by 50.0 bps to 10.75% in February 2025, from 11.25%, and a cumulative 225.0 bps cut from the high of 13.00% in July 2024, signalling easing of policy stance to stir economic activity, noting that its previous measures had contributed to a stronger Shilling and reduced inflationary pressures. Lower interest rates tend to reduce capital inflows as foreign investors demand for local assets reduces, which might put pressure on the Shilling due to limited supply of foreign currency,

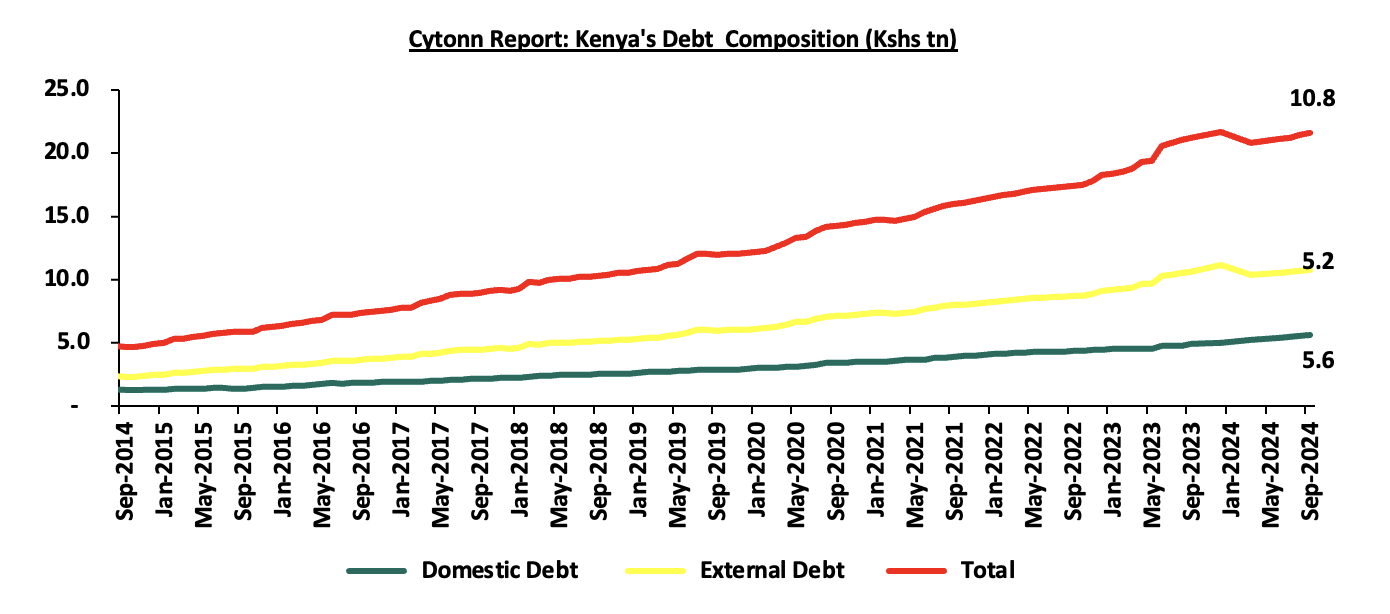

- The high debt levels in the country with the Kenya’s public debt having grown at a 10-year CAGR of 16.2% to Kshs 10.8 tn in September 2024, from Kshs 2.3 tn in September 2014, with external debt accounting for 49.3% of the total debt. This continues to put pressure on our foreign reserves due to the burden of high debt servicing costs and hence continues to weigh down on the Kenyan shilling. The chart below highlights the trend in the country’s debt composition:

Source: CBK

Section II: Evolution of the Interest Rate Environment in Kenya

Interest rates in Kenya are primarily influenced by the Central Bank of Kenya (CBK) through the Central Bank Rate (CBR), which guides the cost of borrowing and liquidity in the economy. The Monetary Policy Committee (MPC) adjusts the CBR based on inflation, exchange rates, and economic growth trends. Commercial banks use this benchmark to set lending and deposit rates, affecting credit availability and overall economic activity.

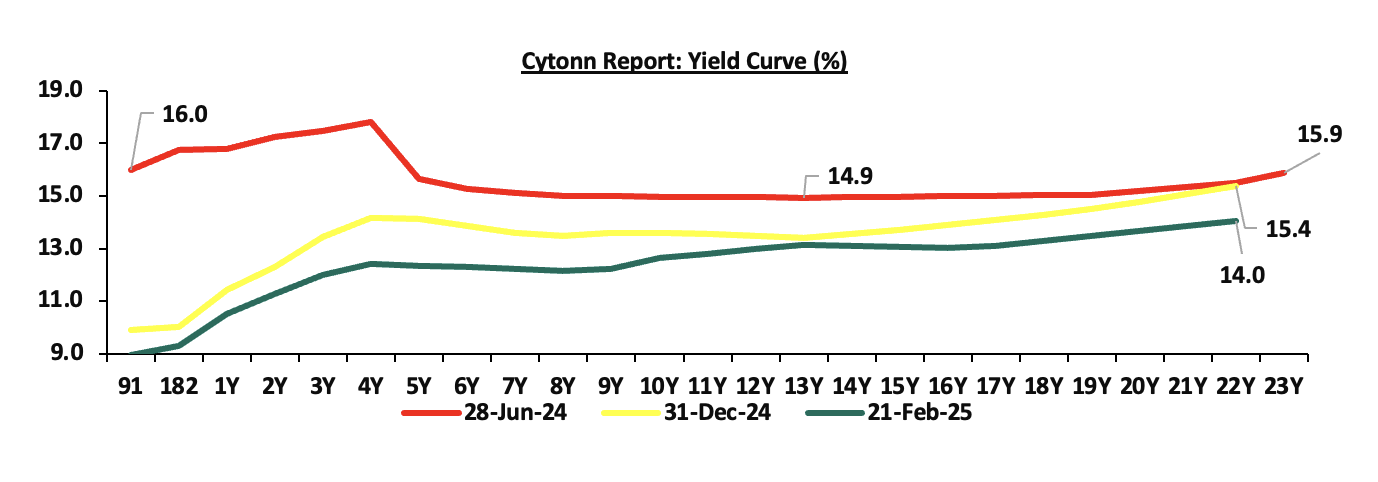

In FY’2024, interest rates faced mixed performance but generally ended the year on a downward trajectory with rates on the 91-day paper falling by 608.8 basis points cumulatively, to close the year at 9.9%, down from the rate of 16.0% recorded at the beginning of the year. However, interest rates recorded highs of 16.0%, 16.9%, and 16.9% for the 91-day, 182-day and 364-day papers respectively in July 2024 before the downward trend. The significant decrease in interest rates is attributed to investors perceiving lower risks due to reduced credit risk on the country, eased inflation, currency appreciation, and improved liquidity positions. During the first half of 2024, the yields on government securities were on an upward trajectory primarily due to the government’s amplified borrowing needs and investors’ pursuit of higher returns to mitigate the impact of the inflation rates observed in the first half of the year. The second half of the year saw a decline in yields as liquidity positions improved and investors demand for the securities improved. Notably, the government’s ability to meet coupon payments and successfully redeem the 10-year Eurobond maturing in June 2024 provided much-needed confidence in Kenya’s fiscal management. The yield curve has since evolved from a humped curve in June 2024, with short- to medium-term yields significantly higher than long-term yields, indicating heightened risk perception and demand for shorter-term securities, to a more normalized yield curve by December 2024, with long term bonds having highest yields. The graph below shows the yield curve over the period:

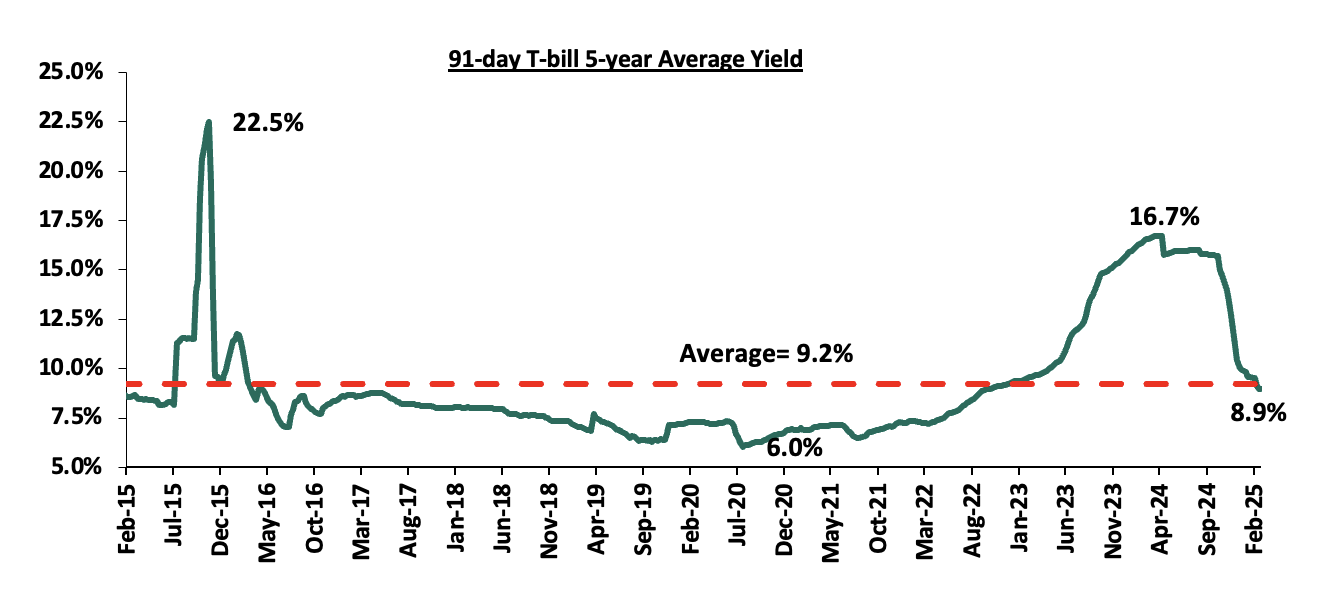

Over the last 10-year yields on government papers have remained steady for the most part, with the yields on the 91-day paper averaging 9.2%. However, Kenya’s interest rates witnessed high volatility in the years 2015 and 2016 and 2024 with the 91-day paper hitting a record high of 22.5% in October 2015 attributed to the tight monetary policy stance adopted by the Central Bank of Kenya, with the Monetary Policy Committee (MPC) raising the CBR to 10.0% in June 2015 from 8.5% in order to anchor inflationary expectations and curtail demand pressures in the economy, and, 16.0% in July 2024, attributable to the tight monetary policy with CBR at 13.0%. However, following an ease in inflationary pressures and a stronger Shilling, the CBK has since adopted an expansionary monetary policy stance by cutting the Central Bank Rate (CBR) and Cash Reserve Ratio (CRR) in a bid to support the economy through reduced cost of borrowing and improved liquidity. The chart below highlights the trend in the 91-day T-bill weighted average yield for the last 10 years:

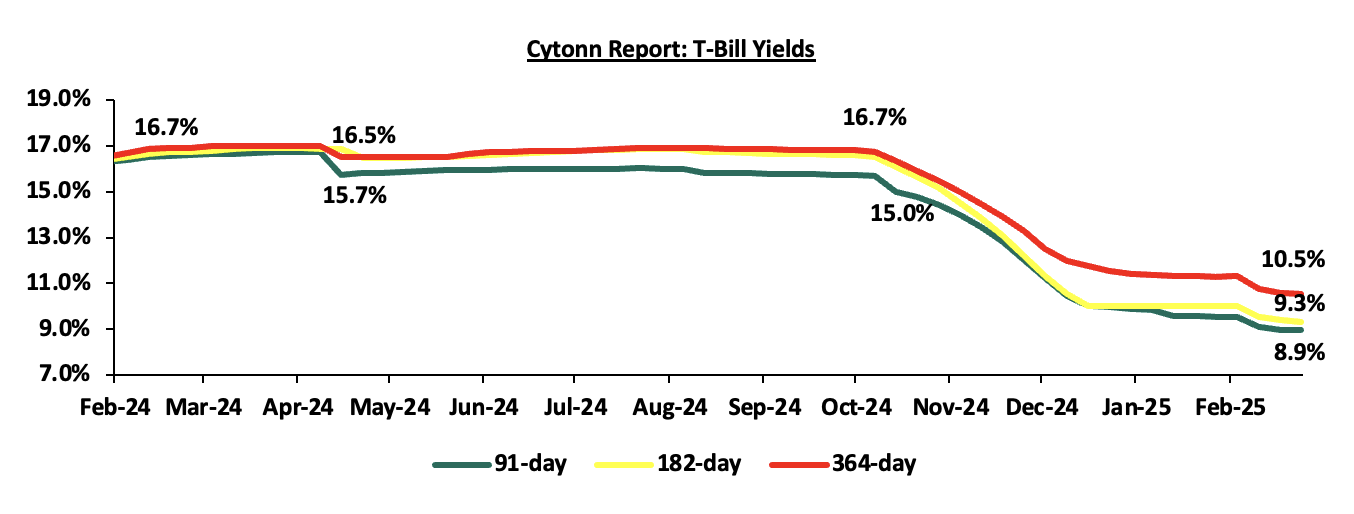

The yields on the government papers continue to decline in 2025, with the yields on the 91-day paper recording a YTD decline of 87.8 bps to 8.9% as of 20th February 2025, from the 9.8% recorded at the start of the year. The yields on the 364-day and 182-day papers have declined by 84.5 bps and 71.4 bps respectively on a YTD basis to 10.5% and 9.3% as of 20th February 2025, from the 11.4% and 10.0% respectively recorded at the start of the year. The chart below shows the yield performance of the 91-day, 182-day and 364-day papers from February 2024 to February 2025:

The Kenyan macroeconomic environment has shown slight improvement mainly as a result of the contained inflationary pressures and appreciation of the Kenyan Shilling that have supported business production levels. Business conditions in the Kenyan private sector recorded an improvement during the year, with the average Stanbic Bank Monthly Purchasing Managers’ Index (PMI) for 2024 averaging at 49.6, 1.5% points higher than the average of 48.1 recorded during a similar period in 2023, and currently at 50.5 as of January 2025, above the expansionary zone of 50.0. Additionally, we expect the reduced borrowing costs to increase lending to the private sector, hence increasing activity and growth in the economy. Despite this, cost of living still remains high in the country partly on the back of increased taxation, impeding on revenue collection and as such, we expect revenue collection to slightly lag behind the revised target. The revised budget expenditure stands at Kshs 4,851.1 bn against revenue collection projection of Kshs 3,115.5 bn for the FY’2024/25.

Despite the ongoing decrease in interest rates, there remains a concern on the sustainability of the lower yields, given the high government debt maturities, which necessitates the government to borrow. Our view is that the government should take the following measures to alleviate the possible strain on the interest rate:

- Shift financing strategies to focus on concessional financing, while limiting the use of commercial borrowing. This approach will help reduce pressure, improving the shilling's appreciation, as concessional funds offer lower interest rates and extended repayment periods,

- Continue to prioritize domestic borrowing in the short to medium term due to the cost advantage of domestic debt over foreign currency-denominated debt. Given the higher interest rates and currency risks linked to external borrowing, domestic financing offers a more economical alternative for the government. The domestic debt to external debt mix stood at 51.9% to 48.1% as of September 2024 a shift from 46.5% to 53.5% in September 2023.

- The government should implement measures to curb corruption, enhance transparency, and strengthen governance structures. A corruption-free environment attracts foreign direct investment, boosts economic efficiency, and reinforces confidence in a stable interest rate environment

- Continue implementing measures to reduce the debt service-to-revenue ratio, which stood at 57.1% as of January 2025, 27.1% points higher than the recommended threshold of 30.0%, and 15.2% points lower than average FY2023/24’s debt service ratio of 72.3%. This decrease is mainly due to efforts to enhance revenue collection, such as broadening the tax base, curbing tax evasion, and suspending tax relief payments, though the government has yet to fully benefit from these strategies,

- Implement measures to attract Foreign Direct Investment (FDI) and strengthen the country’s economic position. A steady inflow of foreign capital boosts foreign exchange reserves, reducing reliance on domestic borrowing and easing pressure on interest rates

- Diversify project funding by eliminating barriers to Public-Private Partnerships (PPPs) and joint ventures. This approach encourages greater private sector participation in financing development projects, particularly in infrastructure, reducing the reliance on extensive government borrowing,

- Control government spending by focusing on core functions and eliminating corruption and wasteful expenditures at both county and central government levels, and,

- Ensure the continuity of macroeconomic stability by controlling inflation and maintaining a stable exchange rate through Central Bank policies that shape the interest rate environment. Prudent monetary policies and effective liquidity management enhance stability and predictability, fostering investor and lender confidence while positively influencing interest rates.

Section III: Currency Outlook

|

Driver |

Outlook |

Effect on the currency |

|

Balance of Payments |

• The improvement of the country’s balance of payments is likely to put less pressure on the shilling. Notably, Kenya’s balance of payment (BoP) position improved significantly by 113.5% in Q3’2024, with a surplus of Kshs 17.8 bn, from a deficit of Kshs 131.5 bn in Q3’2023, and a 78.9% decline from the Kshs 84.1 bn surplus recorded in Q2’2024.This was caused by a significant improvement in the financial account due to the , attributable to increased inflows of debt securities and other investments, in spite of the reduced loan disbursements to general government, a trend likely to continue in 2025. As such, we expect increased foreign direct investment leading to increased inflows and hence supporting the shilling. • We expect the gradual improvement in the export sector as Kenya’s trading partners continue to reopen, seeing the current account deficit coming at 4.0% of GDP in Q3’2024. • However, we expect the country’s reliance on imports coupled with high global commodity prices to continue weighing down on the country’s Balance of payments. However, we expect the stable Shilling to keep the import bill in check. |

Neutral |

|

Government Debt |

• We expect the government to borrow aggressively from the domestic market as it aims to plug in the fiscal deficit, which is projected to come in at Kshs 864.1 bn in the FY’2024/25 Supplementary Budget Estimates II, 4.9% of the GDP. The government intends to plug this fiscal deficit through Kshs 280.1 bn in external financing and Kshs 584.0 bn in domestic borrowing. Borrowing domestically is less costly for the government than acquiring debt denominated in foreign currencies, which not only carry higher interest rates but also come with the added risk of currency fluctuations. • Similarly, we expect the level of foreign borrowing will also increase in 2025 due to the following reasons; (i) Disbursement of concessional loans from the IMF under the Extended Credit Facility arrangement (EFF/ECF) and the Resilience Sustainability Facility (RSF) programme, coupled with funding from the World Bank under the Development Policy Operation (DPO) arrangement, and (ii) Disbursement of commercial loans from commercial lenders such as the Trade & Development Bank (TDB) and the African Development Bank, • The high debt levels will continue to expose the shilling to exchange rate shocks and will, in turn, emanate pressure on the shilling to weaken during the repayment period. |

Negative |

|

Forex Reserves |

• The forex reserves have significantly increased by 28.2% to USD 9.3 bn (equivalent to 4.7 months of import cover) as of 21st February 2025, from USD 7.2 bn (equivalent to 3.8 months of import cover) recorded in a similar period in 2024. The increase is largely attributed to the increased foreign capital inflows. Additionally, we expect the reserves to be supported by improving diaspora remittance inflows which came in at USD 4,960.2 mn in the 12 months to January 2025 which is 16.6% higher than the USD 4,252.9 mn recorded over the same period in 2024 and the increasing exports especially in the agricultural sector with government having subsidized key inputs such as fertilizers. This will in turn support the stability of the Kenyan Shilling • However, we expect the elevated debt levels witnessed in the country to put forex reserves under pressure as most of it will be used to finance the debt maturities,

|

Positive |

|

Monetary Policy |

• Inflation rates have remained within the government’s target of 2.5% - 7.5% for nineteen consecutive months coupled with the stable fuel prices in the country as a result of the previous measures by the MPC to curb inflationary pressures. Notably, in its latest sitting, the MPC lowered the CBR by 50.0 basis points a move which it termed as aiming to boost private sector growth and support economic activity and growth. The impact of this is expected to support economic activity, while still ensuring exchange rate stability. • Consequently, we expect to see continuous downward pressure on the interest rates as the ripple effects of the decreased CBR continue to reflect in economy in the short to medium term. |

Neutral |

From the above currency drivers, 1 is negative (Government Debt), 2 are neutral (Balance of payment and Monetary Policy), while 1 is positive (Forex Reserves) indicating a more stable outlook for the currency.

Section III: Factors Expected to Drive the Interest Rate Environment

- Monetary Policy

The monetary policy committee has continued to play a crucial role in determining the interest rates levels in the country. In 2024, notable changes in interest rates were noted in July when short-term government securities rates peaked at 16.0%, 16.9%, and 16.9% for 91-day, 182-day and 364-day papers respectively. The yields on the short-term papers then began to decline, gaining momentum following the Central Bank's decision to reduce the base lending rate to 11.25% by December 2024, a cumulative 175 .0 bps from the existed 13.00% in July 2024, which saw the rates decline to close 2024 at 9.9%, 10.0%, and 11.4% for 91-day, 182-day and 364-day papers respectively. In its December meeting, the MPC noted that its previous measures had contained inflation which stood at a low of 2.7% as of October 2024, nearing the lower end of the target range of 2.5%-7.5%. In its latest meeting held in February 2025, the MPC cut the CBR further by 50.0 bps to 10.75%. Short-term paper yields declined after the CBK cut the base lending rate to 11.25% by December 2024 175 bps drop from 13.00% in July, closing the year at 9.9%, 10.0% and 11.4% for the 91-day, 182-day and 364-day papers respectively. The MPC attributed the cut in December 2024 to contained inflation, which fell to 2.7% in October 2024, nearing the 2.5%-7.5% target range. In February 2025, the CBR was cut further by 50 bps to 10.75%. The policy rate influences the cost of borrowing for banks and consequently, affects the rates at which they lend to businesses and individuals. This, in turn, creates a ripple effect on the overall interest rate environment, including the yields on government securities. Since then, the rates for short-term government papers have declined, reaching 8.9%, 9.3%, and 10.5% for 91-day, 182-day, and 364-day papers, respectively as of 20th February 2025.

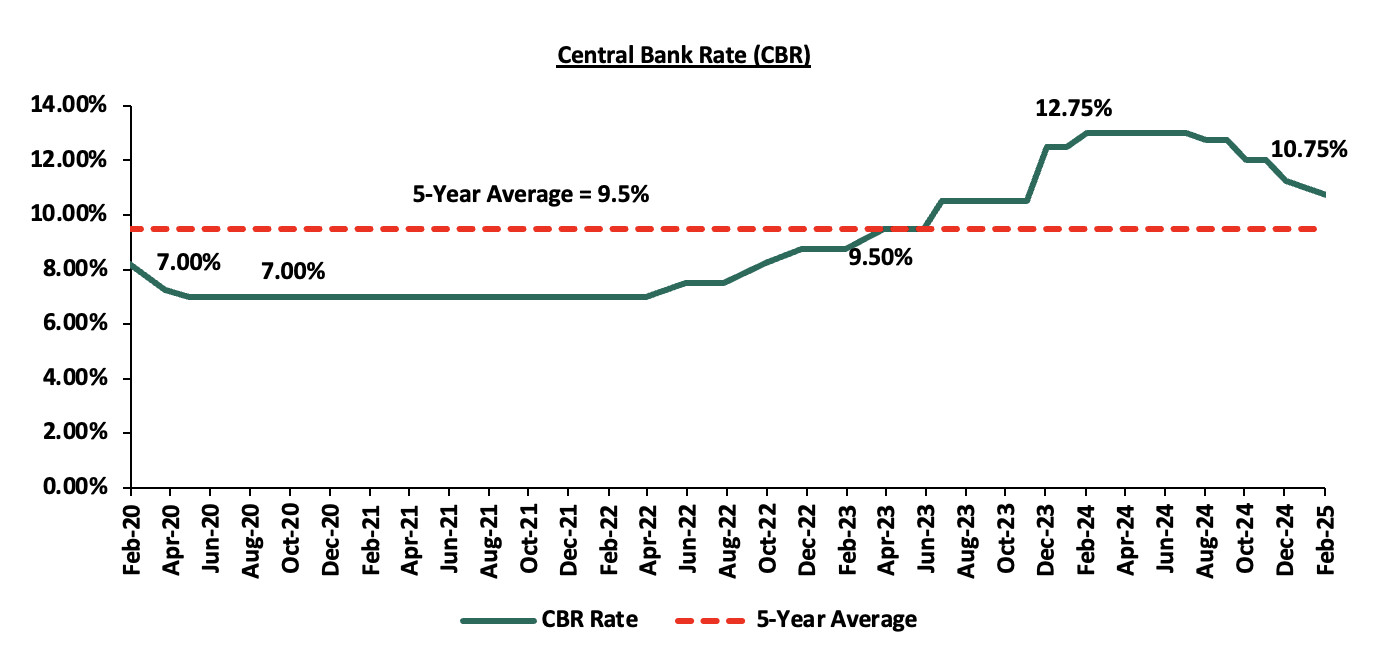

The Central Bank is expected to continue with the expansionary monetary policy stance in the medium term with the intention to revive private sector growth and boost economic activity and has initiated on-site inspections of commercial banks to ensure they reduce lending rates in line with recent monetary policy changes. As such, we expect to see continued downward pressure on the interest rates attributable to investors perceiving lower risks due to eased inflation, currency appreciation, and improved liquidity positions. The following is a graph highlighting the Central Bank Rate for the last 5 years;

Source: CBK

- Fiscal policies

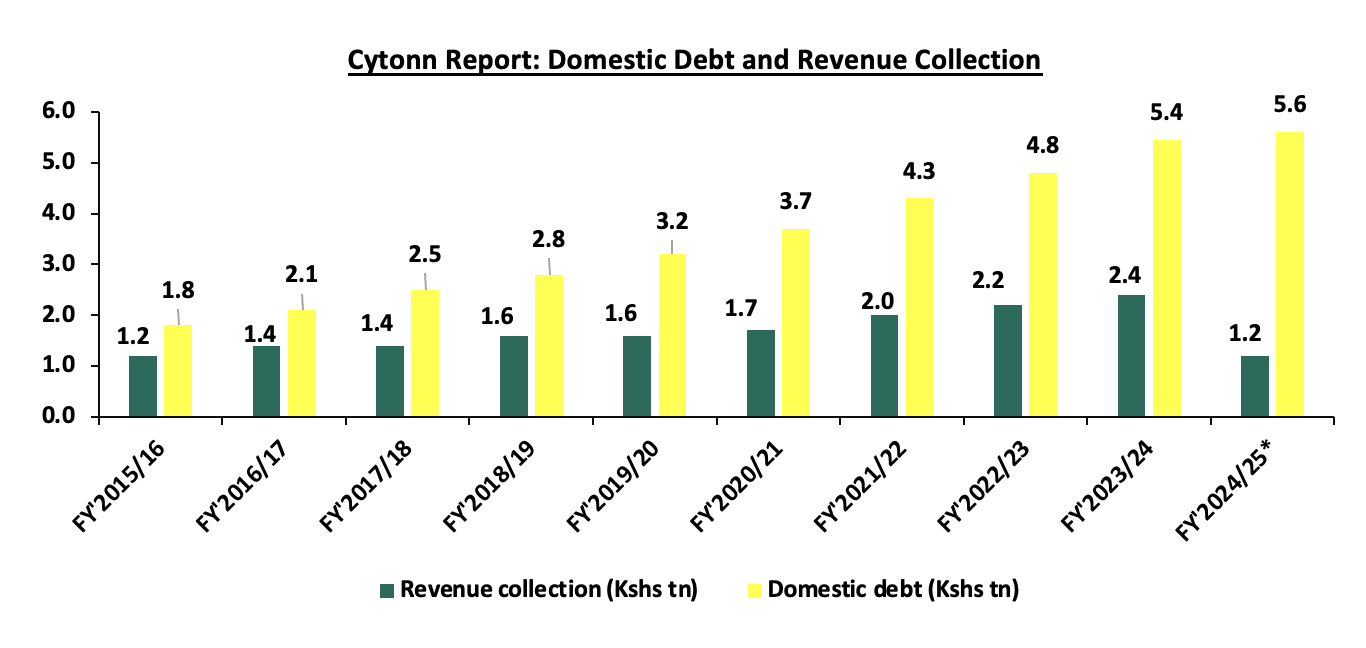

The government continues to put in place measures to broaden the revenue base and rationalize expenditures in order to reduce the fiscal deficits. The FY’2024/25 budget primarily aims to achieve growth-friendly fiscal consolidation by safeguarding the country’s debt sustainability through targeted expenditure rationalization and enhanced revenue mobilization. Notably, the government projects to narrow the fiscal deficit to 4.9% of GDP in FY’2024/25, from the 5.7% of GDP in FY’2023/24. However, the upward revision of taxes comes at a time when the cost of living is high, weighing down on the projected revenue performance. As such, we expect this will significantly affect revenue collection necessitating borrowing to plug in the budget deficit. Below is a chart showing the revenue collections and domestic borrowings over the last 10 financial years:

Source: National Treasury, KRA, * Domestic Debt Figures as of September 2024, *Revenue collection as of December 2024

- Liquidity

The MPC lowered the Cash Reserve Ratio (CRR) to 3.25% from 4.25% in their February 2025 sitting and this marked the first time since March 2020 when the MPC lowered the Cash Reserve Ratio (CRR) to 4.25% from 5.25% aiming to support the economic recovery from the ripple effects of Coronavirus pandemic. The latest cut in February 2025 aimed to support the lowering of lending rates, complement the reduction in the CBR, and address banks’ reluctance to lower their lending rates in line with CBR cuts. By reducing the CRR from 4.25% to 3.25%, the MPC freed up liquidity that banks had previously been required to hold with the Central Bank. This increased the money supply in the interbank market and commercial lending. Liquidity in the money market tightened in 2024, as evidenced by the interbank rates recording an average of 13.0% in 2024, compared to an average of 9.8% in 2023, with average interbank volumes however increasing by 19.1% to Kshs 26.7 bn in 2024, from Kshs 21.6 bn in 2023. In an ideal situation, ample liquidity in the money market, the lowering of commercial banks’ lending rates, and deposit rates would lead to increased money supply in the economy and an increase in consumers’ purchasing power. The low Cash Reserve Ratio has played a big role in maintaining favourable liquidity in the money market as well increases the supply of money by commercial banks. We expect liquidity to improve in 2025 driven by increased access to credit as banks gradually increase their lending to the private sector and the continued adoption of risk-based lending by banks. However, due to uncertainties in the economy, there still exists a high credit risk which hampers lending to businesses and individuals.

Outlook:

|

Driver |

Outlook |

Effect on Interest Rates |

|

Fiscal Policies |

• The government is expected to continue borrowing in order to offset the budget deficit and finance debt maturities. The total T-bonds and T-bill maturities so far stand at Kshs 212.7 bn and Kshs 438.8 bn, respectively for the remaining FY’2024/25 which is likely to put pressure on rates |

Negative |

|

Monetary Policy |

• We expect the MPC to continue with the easing of the monetary policy in the short term in a bid to foster private sector credit growth and support the economy, given that inflation remains within the government’s target and the Shilling has stabilized. This is evidenced by the recent actions taken by the MPC where it reduced the CBR by 50.0 basis points to 10.75% from 11.25%. • As such, the yields on government securities are likely to adjust further downwards as investors attach a lower premium to meet their required real rate of return, |

Positive |

|

Liquidity |

• We expect liquidity to continue being supported by the Low Cash Reserve Ratio (CRR) currently at 3.25% from 4.25% previously. • Additionally, we expect liquidity to improve in 2025 driven by increased access to credit as banks gradually increase their lending to the private sector and the continued adoption of risk-based lending by banks. • The huge maturities from government securities are expected to increase liquidity |

Positive |

From the above indicators, 1 of the drivers is negative (fiscal policies), and 2 are positive (Monetary policies and liquidity). We therefore believe that the interest rate environment remains optimistic and will likely adjust further downwards.

Section IV: Conclusion and Our View Going Forward

Based on the factors discussed above and factoring in the uncertainties in the Kenyan macroeconomic environment;

- We expect the Kenya Shilling to trade within the range of between Kshs 134.4 and Kshs 140.5 against the USD by the end of 2025 based on the purchasing power parity (PPP) and interest rate parity (IRP) approach respectively, with a bias of a 4.6% depreciation mainly driven by:

- The ever-present current account deficit with Kenya being a net importer, which will increase US Dollar demand in the market,

- The low interest rates as evidenced by the expansionary monetary policy stance adopted by the MPC. The lower interest rates will lead to reduced capital inflows as foreign investor demand for local assets reduces, and,

- The persistent US Dollar demand by importers, mainly in the oil and energy sector as well as manufacturers.

- We expect a stability on the yield curve with our sentiments being on the back of the improved liquidity in the money markets, allowing for cheaper borrowing for budgetary support, funding of infrastructure projects, and payment of domestic maturities. Further, we expect the yield curve to normalize in the short to medium- term as the government turns to increased external borrowing alleviating pressure on the domestic market.

Concerns about the future performance of the Kenyan shilling have eased, driven by reduced pressure on the currency and improved foreign exchange reserves. However, the high national debt will continue to exert pressure on the shilling. As we anticipate continued currency stability, economic improvement is expected, reflected in a declining import bill. Despite the implementation of an eased monetary policy, marked by the MPC's reduction of the Central Bank rate to 10.75% in February 2025 from 11.25%, we still expect inflationary pressures to be contained in the short-term, remaining within the CBK’s target range of 2.5%-7.5%. The current stability of the Kenyan shilling is likely to be sustained in the immediate future, contingent on the government’s ability to effect proactive measures that further sustain the strong Shilling. These measures encompass strategic interventions and policies aimed at maintaining the stability of the currency and fostering economic resilience. They include:

- Formulate policies to encourage Foreign Direct Investments (FDIs): The government should prioritize creating an attractive investment environment for foreign investments by improving transparency in all required regulations as well as reducing hurdles in the process. This would include targeting sectors that enjoy global interest like the Renewable Energy sector and Sustainable Energy Development Goals (SEDG), and could include incentives for the same. This would majorly increase the foreign exchange reserves thus reducing the pressure on the foreign currency in the Kenyan markets,

- Promotion of Tourism through Implementing robust marketing campaigns to attract international tourists and enhancing the tourism infrastructure which will help increase the inflow of dollars and hence boost our Foreign Exchange Reserves

- Dramatically cut Spending: The government should contain expenditure by limiting expenditure to the core activities of the government as well as reducing wasteful spending at both the County and Central government levels

- Reduce corruption: The government should adopt measures to reduce corruption, improve transparency, and strengthen governance structures. A corruption-free environment attracts foreign direct investment, enhance economic efficiency, and instils confidence in the stability of the Kenyan Shilling.

- Stimulate the capital markets to attract foreign investors: The government should focus on improving the capital markets by implementing policies that encourage foreign investment, streamlining regulatory frameworks, and introducing investor-friendly initiatives. A vibrant capital market attracts foreign capital as well as enhances liquidity and diversifies investment options, contributing positively to currency stability.

- Maintaining a sustainable debt level: The government should find a harmonious equilibrium between engaging in foreign borrowing to boost foreign reserves and preserving a favourable credit standing with creditors. This delicate balance is crucial for maintaining the country's attractiveness to investors, facilitating capital inflows and financial stability.

- Reduction of commercial loans: There is need for the government to reduce the share of commercial loans in order to reduce debt servicing costs. This is mainly because commercial loans attract higher interest rates as compared to concessional borrowings.

- Building an export-driven economy: The government can do this by formulating and implementing robust export-oriented policies and manufacturing to increase exports aimed at reducing the current account while reducing overreliance on imports to preserve the country’s foreign exchange reserves,

- Alternative projects financing strategies: The government should diversify the sourcing of funding for infrastructure projects in the country to further shift to alternative financing strategies such as Public-Private Partnerships (PPPs), joint ventures and stimulation of the capital markets. This will attract more private sector involvement in funding development projects such as infrastructure instead of borrowing, and,

- Improve the Ease of Doing Business: Improving the ease of doing business will make it easier for entrepreneurs to form business ventures, which will eventually grow, employ people and contribute to tax revenues, and,

- Encourage export and revenue diversification: The government should shift from complete over-reliance on traditional agricultural sector exports like tea, horticulture and coffee, through diversification in promoting value-added processing and manufacturing to increase export revenue. Notably, the manufacturing sector contribution to GDP remains low, coming in at only 8.1% in Q4’2023, hence the government should put in policies to grow the sector like incentives which would in turn increase exports as well as preserving the foreign exchange reserves, aiding in stabilizing the exchange rate.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.